Why Managing Burn is So Important

You need to be reexamining how the economy grinding to a halt will impact your business.

[Author’s Note: This post was written alongside my friends at Geodesic Capital when I was an investor with Geodesic]

The last six weeks felt like years. In just a few short weeks, the investor community quickly pivoted from preaching “grow at all costs” to advising “caution and manage your cash burn.” Companies have been advised to delay payments to vendors, renegotiate real estate contracts with landlords, and unfortunately, cut costs across the board to increase runway to 18–24 months. As Warren Buffett once said, “Cash… is to a business as oxygen is to an individual: never thought about when it is present, the only thing in mind when it is absent.”

Even if you just raised a large round that you thought would last years, you need to be reexamining how the economy grinding to a halt will impact your business. And you can’t just examine first order effects; you need to understand second and third-order repercussions. Not only will your revenue take a hit, but as customer budgets shrink, customers will churn at a higher rate, expansion will become contraction, new customers will be harder to acquire, and contract sizes will decrease. All of the items you are rebudgeting, your customers are too.

To help understand how a business can be impacted, let’s look at a hypothetical company in a few different scenarios. This over-simplified example should illuminate the impact all of these factors can have on a business and hopefully helps underscore the importance of managing cash through this crisis (or future crises).

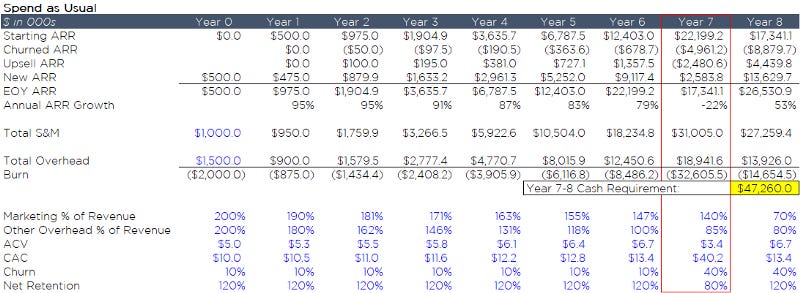

Scenario 1 | Growth Trajectory Without COVID-19

Scenario 1 shows how companies could have grown in upcoming years if a pandemic never occurred — the good old days. This hypothetical software company is on a solid trajectory, growing nicely with solid retention that outweighs churn and an improving overall cost structure. This company expects to need $24m of cash to continue this path during years 7 and 8 of this scenario. Growth is predictable, expenses are justifiable and, let’s face it, raising capital is a fallback if not a milestone. Raising $24m in this environment will be fairly straight forward.

Reaching $67m ARR with fairly efficient growth is sure to land a nice exit for shareholders and probably a massive seed round for this founder’s next venture. Growth trajectories don’t often look this good.

Scenario 2 | The Realities of COVID-19

Unfortunately, we’re living in a new reality. Last year was good and we all took it for granted but there’s no looking back now. In today’s new normal, every company is reevaluating its budget. New customers are likely going to be harder and more expensive to acquire and also likely require discounting to get them over the hump. Also, this company can expect many more customers to churn — be it cost-saving or unfortunately going out of business. In addition, it’ll likely have customers whose usage and seat licenses shrink or may simply bargain for a better price or better payment terms. Expect this year to be ugly.

Scenario 2 shows what happens when companies fail to adjust to the new normal — when they continue to spend and keep their costs structures the same as they would have been in Scenario 1, despite worsening sales efficiency and significantly higher churn. The end result is the company will need twice as much capital in years 7 and 8 while falling $40m ARR short of where they would have under Scenario 1.

Trying to spend through a global economic shutdown might seem like cornering the market, but with so much uncertainty, it’s more likely just swimming upstream. Scenario 2 requires twice as much capital as Scenario 1, despite only achieving half the scale. This puts the company in a forced fundraise situation with minimal growth, high burn, and a potentially-still-recovering economy.

Scenario 3 | Why Extending Runway Matters

Cutting costs, even at the expense of growth, is a requirement and Scenario 3 shows why. As in Scenario 2 of this hypothetical example, it’s year 7 and COVID-19 begins a waterfall of business impacts. New average contract value is again halved from historical normal and customer acquisition cost doubles. But in this scenario, the company cuts customer acquisition channels (marketing) and reevaluates other costs (headcount, real estate, travel, perks). By doing so, it conserves cash through the crisis.

By conserving cash, the topline shrinks but the company minimizes cash outlay. This allows the company to get to $24.5m ARR instead of $26.5m ARR in year 8, but the cash outlay for years 7 and 8 is $17.5m in Scenario 3, instead of $47.3m in Scenario 2. This strategy conserves $30m while ending up just $2m ARR behind. The aggressive way to rebound from this is to think of that $30m as a war chest for year 8 to reaccelerate significantly and surpass Scenario 2’s year 8.

It’s not a pretty ride like Scenario 1, but conserving cash through this downturn is important to survive as well as to come out the other end in a position of strength, ready to capitalize on a potentially more open market. What this is supposed to highlight is the importance of conserving cash during uncertain times. Conserving cash extends the company’s runway and allows the company to bounce back when the situation improves.

Oh, and if you’re curious, assuming the same cash availability as Scenario 2, the steps taken in Scenario 3 enable the company to spend that money later and reach $60m ARR.

Now it’s up to you to determine how your business will be impacted. Your investors and advisors are here to help you uncover blind spots — that is part of why you let them invest and brought them into the family. By working with multiple companies, often in multiple industries, they can help you see around corners you can’t, which may mean the difference between sinking and swimming.